QSR:TSX Stock Forecast (Buy or Sell) for (n+4 weeks)

B. Hedges of net investment in foreign operations Fvtpl ifrs 9 Two methods of recording, including: fair value through profit or loss (“FVTPL”), and amortize cost. Financial liabilities held for trading are measured at FVTPL, and all other financial liabilities are measured at amortized costs unless the fair value option is applied.Investments in equity instruments are financial assets because they are

The standard will have the biggest impact for financial institutions, although some insurers have the option to delay its implementation until the new insurance standard, IFRS 17 comes into effect in 2021. Extinguishment accounting Meanwhile, IFRS 9 prohibits the recycling of gains and losses in OCI to profit or loss in subsequent periods (paragraph 5.7.9 of IFRS 9). We are concerned about this prohibition for the following reasons.

Fair Value Measurements and Hedge Effectiveness

Official Website for the City of Oakland | Mayor Sheng Thao Development Projects De la Torre, Augusto, Alain Ize, and Sergio L. Schmukler. 2012. “Financial Development in Latin America and the Caribbean: The Road Ahead.” Policy Research Working Paper 2380, World Bank, Washington, DC.Under ifrs assets are classified as

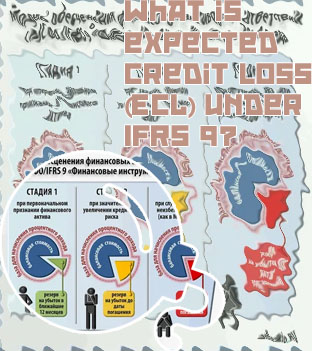

Stage 1 – When a loan is originated or purchased, ECLs resulting from default events that are possible within the next 12 months are recognised (12-month ECL) and a loss allowance is established. On subsequent reporting dates, 12-month ECL also applies to existing loans with no significant increase in credit risk since their initial recognition. Interest revenue is calculated on the loan’s gross carrying amount (that is, without deduction for ECLs). History of IFRS 9 A financial liability should be removed from the balance sheet when, and only when, it is extinguished, that is, when the obligation specified in the contract is either discharged or cancelled or expires. Where there has been an exchange between an existing borrower and lender of debt instruments with substantially different terms, or there has been a substantial modification of the terms of an existing financial liability, this transaction is accounted for as an extinguishment of the original financial liability and the recognition of a new financial liability. A gain or loss from extinguishment of the original financial liability is recognised in profit or loss.